Your car’s in the shop. The clock’s ticking. Do you wait around carless or rent something to stay on the move? And if you do rent, does car insurance cover rental cars for repairs? Can you drive with confidence, or will it cost you double?

You’re not alone if you’re confused. Rental-related insurance claims have jumped recently, while the overall market is expected to reach $62.95 billion by 2025. With such growth, mistakes cost more than ever.

But no worries, we’re here to cut through the confusion.

In this blog, we’ll unpack what your insurer covers, when rental reimbursement applies, what exclusions to watch out for, and how credit cards fit into the puzzle. No fluff, just clarity.

Ready to take the wheel on rental car coverage? Let’s dive in and make sense of it all!

What Is Rental Reimbursement Coverage?

Rental reimbursement coverage is an optional add-on that you can add to your car insurance. It helps pay for a rental car if your car is being repaired because of a covered event, like an accident, theft, or vandalism.

Basically, it helps you to stay on the move while your car gets fixed.

Here’s how it works: if your car is damaged in a covered incident and is unable to be driven, this coverage pays for a rental car.

Most plans cover up to $25–$50 a day for about 30 days, or until you hit a total limit (usually $750–$1,500). If the rental costs more than the daily limit, you’ll have to pay the rest.

The upside is that there’s usually no deductible for rental reimbursement coverage. But remember, if your car needs repairs, the main insurance claim (under collision or comprehensive) will still have a deductible for you to pay.

You can rent from any company, but many insurers have partnerships with preferred rental agencies, so they’ll handle the bill directly. If you go with someone outside their network, you’ll likely have to pay upfront and get reimbursed later.

Important to know: this coverage only works if your car is in the shop for repairs from a covered claim. It doesn’t cover rentals for routine maintenance, mechanical problems (unless you have specific mechanical breakdown coverage), or personal use.

Since it’s optional, you’ll need to add rental reimbursement coverage to your policy and pay a small extra premium. It’s usually pretty affordable and can be very useful if you rely on your car every day.

When Does Car Insurance Cover Rental Cars for Repairs?

Car insurance covers rental cars for repairs only if your car is being fixed for something covered by your policy. This includes accident, theft, vandalism, or certain natural disasters (as long as you have comprehensive and collision coverage).

For example, if you get into a car accident and your vehicle needs repairs, rental reimbursement coverage can cover the cost of a rental while yours is in the shop.

Similarly, if your car is stolen or vandalized and you need a rental during repairs, this coverage may apply.

However, insurance generally does not cover rental cars if your vehicle is in the shop for routine maintenance, mechanical breakdowns, or wear and tear, unless you have purchased specific mechanical breakdown insurance.

This is a common misconception, so double-check your policy to be sure.

Another key point is that rental reimbursement coverage is usually an optional add-on.

If you don’t have it included in your policy, your insurance likely won’t pay for a rental car during repairs, even if you have comprehensive and collision coverage.

Once your claim is approved, rental reimbursement only covers up to a certain daily limit and for a specific number of days (or a max dollar amount).

If your repairs take longer than expected or you rent a car that costs more than your coverage limit, you’ll be responsible for the additional costs.

Some insurers work with specific rental car companies, so they might handle the bill directly for you. But if you rent from a company outside their network, you may need to pay first and then submit receipts for reimbursement.

Bottom line: Check your policy, know your limits, and don’t assume everything’s covered!

To make it easier, here’s a quick table to break it all down for you:

At-a-Glance: Rental Car Insurance Coverage for Repairs

Situation | Covered? | Details |

Accident (your fault or not) | Yes, if you have rental reimbursement coverage | Insurance pays for rental while your car is in the shop. |

Theft or vandalism | Yes, with comprehensive coverage | Rental may be covered during the claim process |

Natural disasters (hail, floods, fire, etc.) | Yes, with comprehensive coverage | Coverage depends on your specific policy. |

Mechanical breakdowns or maintenance | No, unless you have mechanical breakdown insurance | Regular wear-and-tear repairs aren’t covered. |

Disclaimer: This section provides general information only. Rental car coverage during repairs depends on your insurer, policy, and claim details. Always check your insurance policy, rental agreement, and confirm coverage with your insurer or rental company.

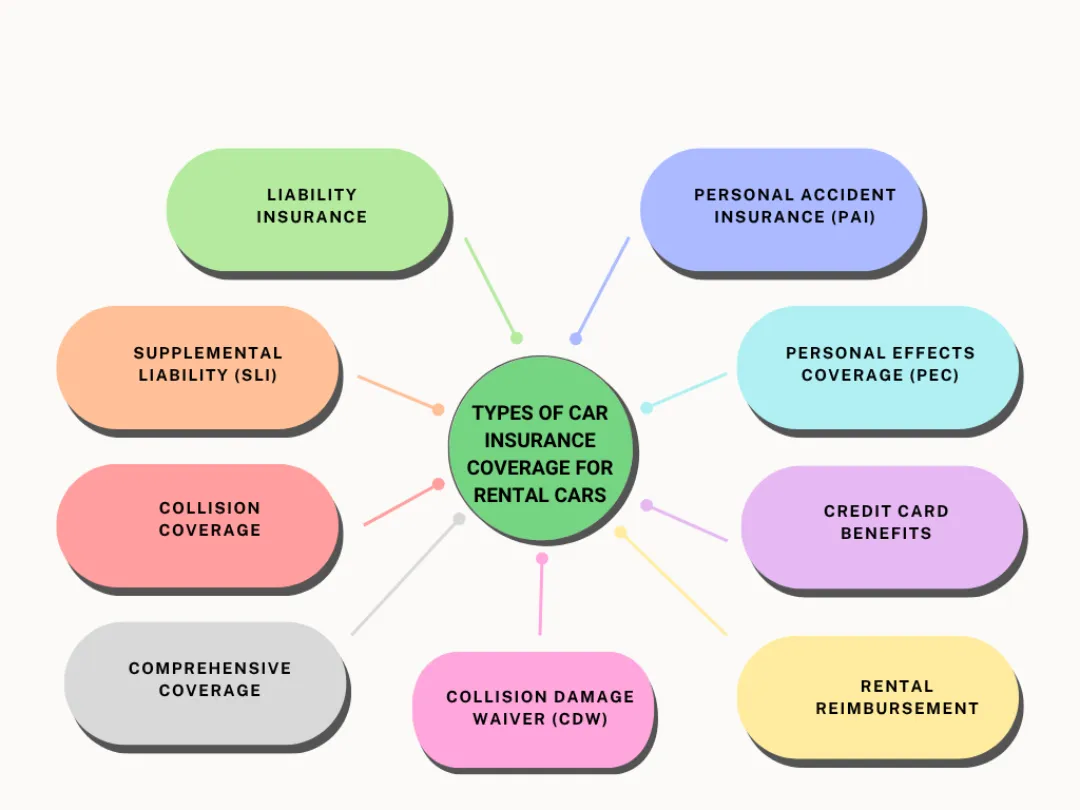

What Types of Car Insurance Coverage Apply to Rental Cars?

Renting a car? Let’s talk about insurance so you’re not caught off guard. Here’s what you need to know.

First, insurance can come from your auto insurance, the rental company, or even your credit card benefits. Each one helps protect you in different ways.

Liability insurance is legally required and covers damage or injuries you cause to others. If your auto policy includes liability, it usually extends to rental cars. Rental companies may offer Supplemental Liability Insurance (SLI) to boost those limits.

Collision coverage covers repair costs for the rental car, no matter who is at fault. If you have it on your policy, it usually applies to rentals, sparing you major repair costs.

Comprehensive insurance covers damage from non-collision incidents such as theft, vandalism, or weather-related events.

Collision Damage Waivers (CDWs) aren’t technically insurance, but they waive your responsibility for damage or theft as long as you follow the rental agreement. If you’re already covered, a CDW may not be necessary, but it could help you avoid out-of-pocket surprises.

Optional extras include Personal Accident Insurance (PAI) for medical costs and Personal Effects Coverage (PEC) for your belongings. If you already have health or renters insurance, these might not be necessary.

Many credit cards offer secondary coverage, which can help with collision and theft after your policy applies. However, they rarely cover liability or injuries, so check your card’s terms before relying on it.

If you have rental reimbursement coverage, it pays for a rental car while your own is being repaired from a covered claim.

If you claim a rental car, you’ll still need to pay your collision or comprehensive deductible, just like with your car. Also, remember that your policy limits for a rental are the same as for your car; they won’t be higher.

Rental Car Coverage Comparison

Coverage Type | Who Provides It | What It Covers |

Liability Insurance | Personal Auto Policy / Rental Co. | Damage or injuries you cause to others |

Supplemental Liability (SLI) | Rental Company | Boosts liability limits above your policy’s basic coverage |

Collision Coverage | Personal Auto Policy | Damage to the rental car, regardless of fault |

Comprehensive Coverage | Personal Auto Policy | Theft, vandalism, weather, and other non-collision events |

Collision Damage Waiver (CDW) | Rental Company | Waives your financial responsibility for damage/theft, not technically insurance |

Personal Accident Insurance (PAI) | Rental Company | Covers medical costs for you and passengers |

Personal Effects Coverage (PEC) | Rental Company | Covers personal belongings in the car |

Credit Card Benefits | Your Credit Card | Secondary collision and theft coverage rarely includes liability |

Rental Reimbursement | Personal Auto Policy | Pays for a rental car while your car is being repaired |

Situations Where Insurance Does Not Cover Rental Cars

Auto insurance often extends to rental cars, but there are plenty of situations where coverage may not apply.

For example, if your car is in the shop for something like a mechanical issue or routine maintenance, your standard insurance typically won’t pay for a rental unless you have specific mechanical breakdown insurance.

Without rental reimbursement coverage added to your policy, your insurer won’t pay for a rental car during repairs, even if the damage is due to a covered claim.

This optional coverage must be added in advance to apply in these situations.

Additionally, if your auto insurance has expired, been canceled, or lapsed, you’re not covered for rental cars. Driving without insurance is risky, illegal, and can lead to big trouble.

If you rent a car for purposes outside your policy terms, like commercial use or allowing unlisted drivers to operate it, your coverage might be void.

Similarly, driving outside the geographic limits specified in your policy can leave you without protection.

Insurance won’t cover damages from activities like off-road driving, racing, or driving under the influence. Both personal insurance and rental coverage also exclude intentional damage or reckless behavior.

Personal items left in the rental car? Not covered by most auto insurance or rental reimbursement policies.

Medical bills for you or your passengers? Likely not covered either, unless you’ve got specific personal accident insurance for that.

Lastly, if a rental car is damaged and taken out of service, “loss of use” fees or administrative charges may apply. These fees are often excluded from personal insurance policies or credit card coverage. So, getting extra insurance from the rental company could be a safer option.

At-a-Glance: Rental Car Insurance Exclusions

Situation | Coverage Status | Key Notes |

Mechanical breakdown/maintenance | Not covered without added coverage | Rental reimbursement or mechanical breakdown insurance is required |

No active auto insurance | No coverage | Driving uninsured is illegal and risky |

Commercial/business use | Usually excluded | Requires separate commercial coverage |

Unauthorized drivers | Coverage void | Only listed drivers covered |

Outside geographic limits | No coverage | Must stay within the policy’s specified area |

Off-road, racing, DUI, reckless | Excluded | Intentional or illegal acts void coverage |

Personal belongings | Not covered | Renters/homeowners insurance may apply |

Medical expenses | Not covered | Personal accident insurance is needed |

Loss of use/admin fees | Usually excluded | Rental company insurance may cover these fees |

Luxury/specialty/long-term rentals | Often excluded | Additional coverage is often required |

Disclaimer: This information is for general guidance and may not cover all scenarios or policies. Always review your specific insurance and rental agreements for exact coverage and exclusions. Consult your insurer or rental company for complete details.

Optional Coverage for Non-Accident Repairs

Not every trip to the repair shop comes from an accident. If your car breaks down or needs regular maintenance, your standard auto insurance probably won’t pay for a rental car unless you’ve got something extra like Mechanical Breakdown Insurance (MBI).

MBI is an optional policy, often available through your insurer or third-party providers. It helps pay for unexpected mechanical failures like transmission or electrical problems.

Some MBI plans even cover rental cars while your vehicle is being repaired, but this usually works only for newer cars and may have mileage limits.

If your insurance or credit card doesn’t cover rentals for non-accident repairs, you can get extra protection from the rental company.

If a rental car gets damaged and can’t be used, you might be charged fees like “loss of use” or admin fees. Regular car insurance or credit card benefits usually don’t cover these, so getting a rental company’s waiver (like CDW or LDW) can be a good backup option.

A Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW) means you won’t have to pay for damages or theft of the rental car. Supplemental Liability Insurance (SLI) increases your liability coverage limits.

There’s also Personal Accident Insurance (PAI) that covers medical expenses, and Personal Effects Coverage (PEC) protects your belongings inside the rental.

These extra options can make life easier, especially when dealing with breakdowns that fall outside typical auto insurance coverage.

How to Check Your Coverage & Avoid Rental Surprises

Before you find yourself stuck at a repair shop wondering whether your rental car is covered, take a few moments to get familiar with your policy.

The easiest way to check is by reviewing your declarations page or logging into your insurer’s mobile app. Look for terms like rental reimbursement coverage, transportation expense, or loss of use. These indicate whether you’re covered and for how much.

If the policy language feels vague or overwhelming, don’t hesitate to call your insurer’s customer service or your agent directly.

Ask pointed questions like, “Will my policy cover a rental car if my vehicle is in the shop?” or “Do I have coverage for non-accident repairs?” Getting answers straight from the source can clear up a lot of assumptions.

Also, be sure to check your daily and total rental limits. Most insurers cap coverage at around $30 per day for a set number of days. If your rental costs more, that difference comes out of your pocket.

Some insurance providers work with preferred rental companies, so if you book through them, billing might be direct, and no upfront payments are needed.

If you go outside that network, you’ll likely need to pay first and request reimbursement later.

And here’s something many overlook: keep your auto policy active and current. Any lapse in coverage could leave you completely unprotected, even if the event would normally be covered.

It’s also smart to revisit your coverage annually. Life changes, and so do driving habits. What worked for you last year might not be enough now.

If you manage multiple rentals or need an easy way to track coverage and claims, rental management tools can simplify everything. They help with rental agreements, insurance tracking, and handling damages, saving you time and hassle.

Conclusion

That’s a wrap on does car insurance cover rental cars for repairs? From rental reimbursement to loss-of-use gaps, we covered it all. If your car ever ends up in the shop, you’ll now know exactly where you stand.

But don’t stop at knowing. The smartest drivers take action, updating their coverage, asking better questions, and avoiding assumptions that could cost hundreds. Insurance is a safety net, not a mystery. You’ve got this.

FAQs

No, rental reimbursement coverage doesn’t cover mechanical breakdowns or routine maintenance. It only applies when your car is in the shop for repairs due to a covered event like an accident, theft, or vandalism.

Yes! If your car is stolen and you have rental reimbursement coverage, it can pay for a rental car while your claim is processed and your vehicle is repaired or replaced.

If you have collision coverage or purchase a Collision Damage Waiver (CDW) from the rental company, damage you cause to the rental car is usually covered. Without this, you might be responsible for repair costs.

Without rental reimbursement, you’ll need to pay out of pocket for a rental car while your vehicle is repaired, unless your personal insurance or credit card offers some form of rental coverage.